Why There Hasn't Been a ChatGPT Moment Yet in Manufacturing

The Invisible Kernel War Between the U.S. and China and the Race to Industrial AI

The Missing Breakthrough

Artificial intelligence has transformed writing, art, and coding. Yet the same revolution has barely touched manufacturing.

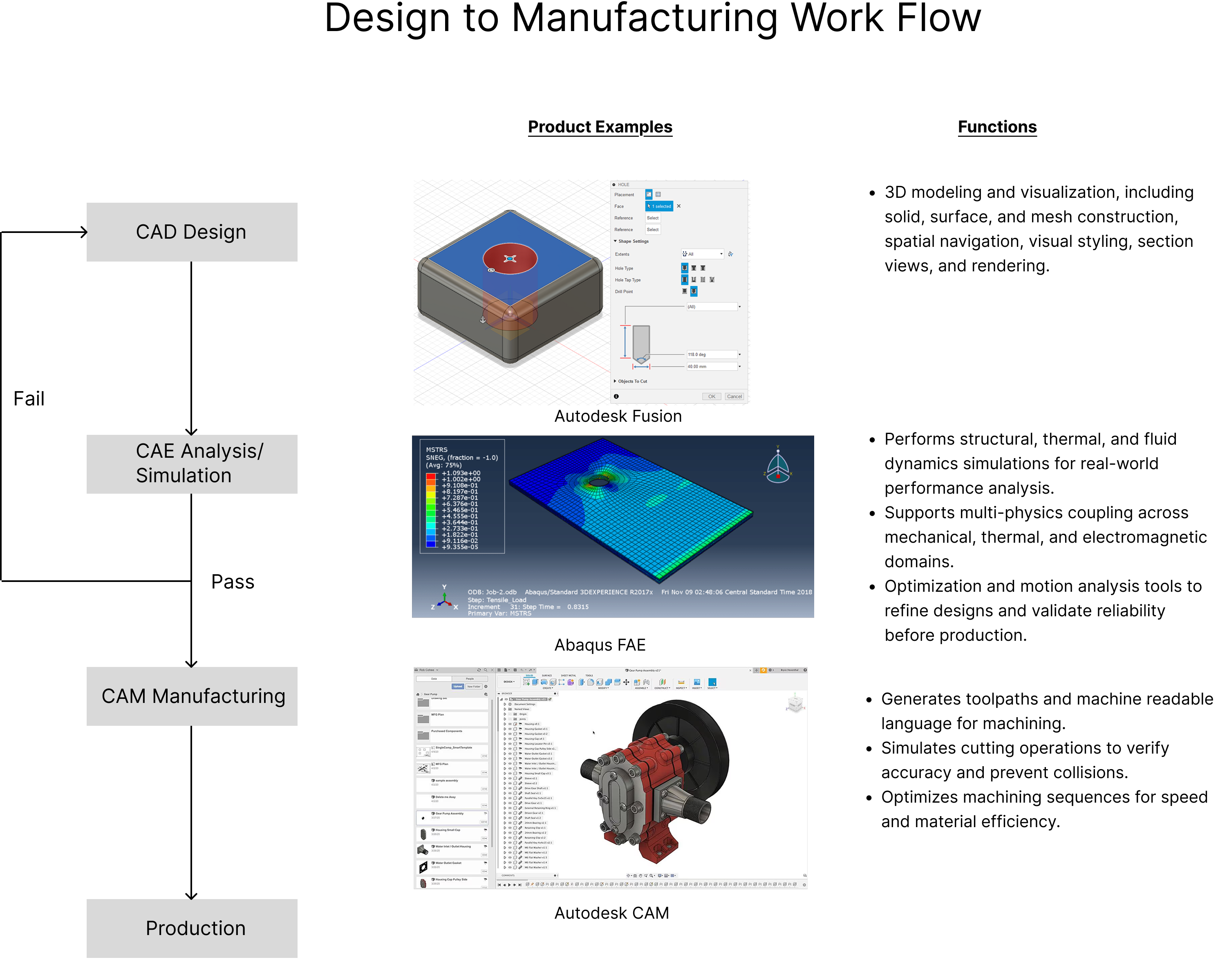

In my previous essay, “We Are Building the Wrong Factories,” I pointed out that understanding manufacturing bottlenecks requires looking at the entire process, from initial design through production, and understanding what the biggest choke points are along the process. The factory floor is only part of the story. To understand why AI has failed to reshape manufacturing the way it reshaped knowledge work, we need to examine the software layer where physical products begin: the design tools themselves.

A mechanical engineer designing a turbine blade in 2025 uses essentially the same workflow as their predecessor in 1995: opening CAD software, manually sketching constraints, defining features one by one, and exporting files through a chain of disconnected tools.

A “ChatGPT moment” for hardware design and manufacturing has yet to arrive. The smart factories envisioned by Industry 4.0 advocates, where design, simulation, and production flow as one continuous system, remain largely theoretical in practice. If AI can generate functioning code, photorealistic images, and coherent essays, why can’t it design a bracket or optimize a gear assembly?

The answer lies in an infrastructure layer most people have never heard of: the geometry kernel.

What Is a Geometry Kernel?

Before exploring why AI struggles with manufacturing, it helps to understand what happens when an engineer creates a 3D model.

When you draw a circle in CAD software, you’re not creating pixels on a screen. You’re defining a mathematical object: a curve with specific geometric properties, constraints, and relationships to other shapes. The software that manages these mathematical definitions, calculating how surfaces intersect, how volumes are created, and whether geometries are valid, is called a geometry kernel.

Think of it like the rules that govern how LEGO bricks snap together. Just as LEGO bricks can only connect in specific ways determined by their geometry, a geometry kernel defines the rules for how digital shapes can be created, modified, and combined. It ensures that a cylinder can intersect with a cube in a mathematically valid way, that two surfaces can be joined without gaps, and that a solid object remains solid when you cut a hole through it. It’s the foundation beneath every 3D model ever created in industrial CAD systems.

Today, virtually all commercial CAD systems are built on a small handful of proprietary kernels monopolized by four companies1.

This concentration has created distinct industry patterns. Aerospace relies heavily on CATIA, automotive on both CATIA and NX, while small-to-medium manufacturers standardize on SolidWorks2. These preferences have solidified as companies accumulated design libraries that lock them into specific kernel architectures.

The Interoperability Gap

The geometry kernel matters because modern manufacturing isn’t a single, integrated process but rather a collection of disconnected stages, each using different software that must translate between incompatible formats.

Imagine you’re working on a document. You start in Microsoft Word, save it as a .docx file, then email it to a colleague who only has Google Docs. They convert it, and some formatting breaks—fonts change, images shift, comments disappear. They make edits and send it back as a PDF. You convert the PDF back to Word to continue editing, but now the text boxes are images and the tables have lost their structure. You fix what you can and export it to PowerPoint for a presentation. The bullet points don’t transfer cleanly, so you recreate them manually. Each conversion loses information. Each handoff requires human intervention to repair what the translation broke.

Now imagine that workflow, but instead of a document, it’s a turbine blade worth $50,000. And instead of formatting errors, the “bugs” are tolerance stackups that cause mechanical failures or manufacturing defects that not only ruin expensive materials but can lead to catastrophic failures when the part is put into service. Unlike software bugs that can be patched with an update, manufacturing errors are irreversible and costly.

A typical workflow begins when an engineer designs a part in CAD software. To test it under stress, they export to simulation software, losing geometric detail in translation. The analyst runs simulations and returns static reports. Once approved, a manufacturing engineer imports the geometry into CAM software to plan toolpaths, again translating formats and potentially losing tolerance or material data. The final output is G-code that factory machines execute. If a part fails during production, this entire chain runs in reverse through each handoff.

This fragmentation is why AI struggles to learn from manufacturing data. Instead of a unified dataset connecting design decisions to production outcomes, there are scattered files, inconsistent metadata, and countless human interventions. What appears to be a digital process is actually a collection of isolated silos that rarely communicate.

The Moat: Why This Problem Persists

If this fragmentation is so problematic, why hasn’t it been solved?

The companies controlling geometry kernels have built formidable moats from decades of real-world validation, institutional trust, and economic lock-in.

Since the 1980s, every aircraft fuselage, automotive chassis, and turbine blade has passed through one of these proprietary kernels. Entire industries have built their design libraries, supplier networks, and manufacturing workflows around them, absorbing millions of hours of engineering testing and production feedback. Tens of millions of legacy 3D models depend on their exact geometry definitions.

Switching to a new kernel would mean rebuilding every legacy part file, rewriting thousands of third-party plug-ins, and retraining engineers worldwide. For companies like Boeing or General Motors with decades of accumulated design data, such transitions are effectively impossible.

The moat is also financial. Licensing these kernels costs software developers thousands to tens of thousands of dollars per seat annually, with additional runtime royalties for each end-user installation. The exact prices of geometry-kernel licenses are not publicly disclosed, but the cost can be inferred from the licensing structures of commercial CAD software that use them. These fees compound quickly for any company building CAD software at scale, creating prohibitive barriers for startups, university labs, and smaller companies.

Open-source alternatives like Open Cascade exist but struggle to gain industrial traction. Performance remains a challenge: boolean operations that take seconds in commercial kernels can take minutes in Open Cascade. More fundamentally, these alternatives face a validation paradox: without decades of production use, they cannot achieve battle-tested reliability; without proven reliability, they cannot access real manufacturing workflows. A single geometric error can cause assembly failures or expensive machine crashes. For companies operating on tight tolerances and thin margins, such uncertainty is unacceptable.

This creates a self-reinforcing cycle. The established kernels carry the institutional trust and accumulated knowledge of forty years of industrial use, backed by billions of dollars in legacy infrastructure. New entrants cannot easily break in, even if their technology is theoretically superior.

Why This Matters for AI

This legacy infrastructure is the primary barrier preventing AI from transforming manufacturing the way it has transformed creative and knowledge work.

Modern AI models learn from data. ChatGPT learned from billions of text documents. Midjourney learned from millions of images. But manufacturing AI has no equivalent training corpus. Design files are locked in proprietary formats. The connections between design decisions, simulation results, and production outcomes are trapped in disconnected systems. The feedback loops that would teach AI what works and what fails are severed by format conversions and manual handoffs.

Even when AI generates promising designs, and systems like generative design algorithms can already optimize shapes for weight, strength, or material efficiency, those designs must still pass through the closed gates of proprietary geometry kernels to become manufacturable parts that the industrial world will accept.

Most AI CAD startups today are building application layers on top of existing infrastructure. Bench automates design workflows across existing CAD and CAE tools but depends on those underlying systems. Leo AI provides an engineering copilot for technical answers and concept generation, but outputs must be realized through traditional CAD software. These tools add value, but they’re ultimately constrained by proprietary kernels. They can make existing workflows faster or more intelligent, but they cannot fundamentally reimagine how geometry is created, validated, and manufactured. This matters because the real prize isn’t incremental efficiency, it’s collapsing the design-to-production cycle from months to days, enabling mass customization at scale, and allowing smaller companies to compete without armies of CAD engineers. That transformation requires rebuilding manufacturing from the geometry up, not just adding AI features to legacy workflows.

A true breakthrough would require an AI system that understands geometry, materials, physics, and manufacturing constraints simultaneously. Such a system would need to:

Generate parametric designs that engineers can edit, refine, and adapt—not just static meshes

Integrate physics and manufacturing constraints in real time, ensuring every design is buildable, not just aesthetically interesting

Plan production automatically, translating models into toolpaths, machine selections, and cost estimates

Learn from production feedback, improving with each cycle as factories return real-world performance data

This would represent the transformation manufacturing needs: when AI designs with precision and manufacturability, not just inspiration.

But building this system requires open access to the geometry layer. Without it, AI remains locked out of the industrial core.

The Strategic Competition

The geometry kernel problem is not just a technical challenge but also a strategic competition between industrial powers.

United States: Incremental Innovation Within Proprietary Systems

In the United States, both established companies and startups are working toward AI-integrated design systems. Autodesk has announced research into neural CAD models trained on mechanical geometry. PTC’s cloud-based Onshape platform is experimenting with AI assistants for feature editing. Siemens has partnered with Microsoft to explore connections between design tools and factory automation. Notably, these incumbents control their own geometry kernels, giving them privileged access to integrate AI at the foundational layer.

More recently, a wave of startups has emerged to tackle this problem more directly. Atomic Industries is building AI-powered systems for injection mold tooling, applying foundational models to one of manufacturing’s most critical and complex domains. Spectral Lab is developing generative models for mechanical components, training AI to understand manufacturing constraints from the ground up. Dirac Inc is working on AI-driven CAD tools that aim to bridge the gap between CAD design and production-ready geometry. While these startups represent promising directions, they remain early-stage efforts navigating the same fundamental constraint: dependence on proprietary geometry kernels.

*Video demonstrates how Dirac Inc’s BuildOS automatically translates complex CAD files into a logical assembly plan by grouping repetitive parts into kits and defining efficient, relationship-based subassemblies, ensuring the animated build sequence updates instantly with design changes.| Source: Dirac Inc

These efforts have been enabled in part by the release of large-scale 3D geometry datasets. NYU released the ABC Dataset, a collection of one million CAD models for geometric deep learning research. Autodesk released the Fusion 360 Gallery Dataset, containing over 8,600 parametric CAD models with rich 2D and 3D geometry data from real user designs. These datasets give AI systems something substantial to learn from. But there’s a critical limitation: most available datasets consist of synthetic models, academic examples, or simplified parts that have never been manufactured. They lack the manufacturing annotations, tolerance specifications, material properties, and production feedback that distinguish a real industrial part from a 3D shape.

This is why the initial training dataset matters so much. An AI trained on synthetic geometry might generate designs that look plausible but fail in production—parts that can’t be machined with standard tools, assemblies with impossible tolerance stackups, or components that seem optimal until they encounter real-world stresses. Without access to authentic manufacturing data, AI systems remain untethered from physical reality. They need designs that have been built, tested, failed, and refined through actual production cycles.

The companies that succeed will be those that can access or generate real production data at scale, creating feedback loops where AI learns not just from what designs look like, but from what actually works on the factory floor.

Yet even with better datasets, progress remains constrained. The foundational layer, the geometry kernel, remains controlled by the same proprietary systems that have dominated for decades, systems that were never architected to integrate with AI.

China: Building an Integrated Stack from the Ground Up

China, meanwhile, is pursuing a fundamentally different strategy: building an integrated stack from the ground up where government policy, domestic kernel development, and industrial AI deployment reinforce one another.

National Industrial Policy

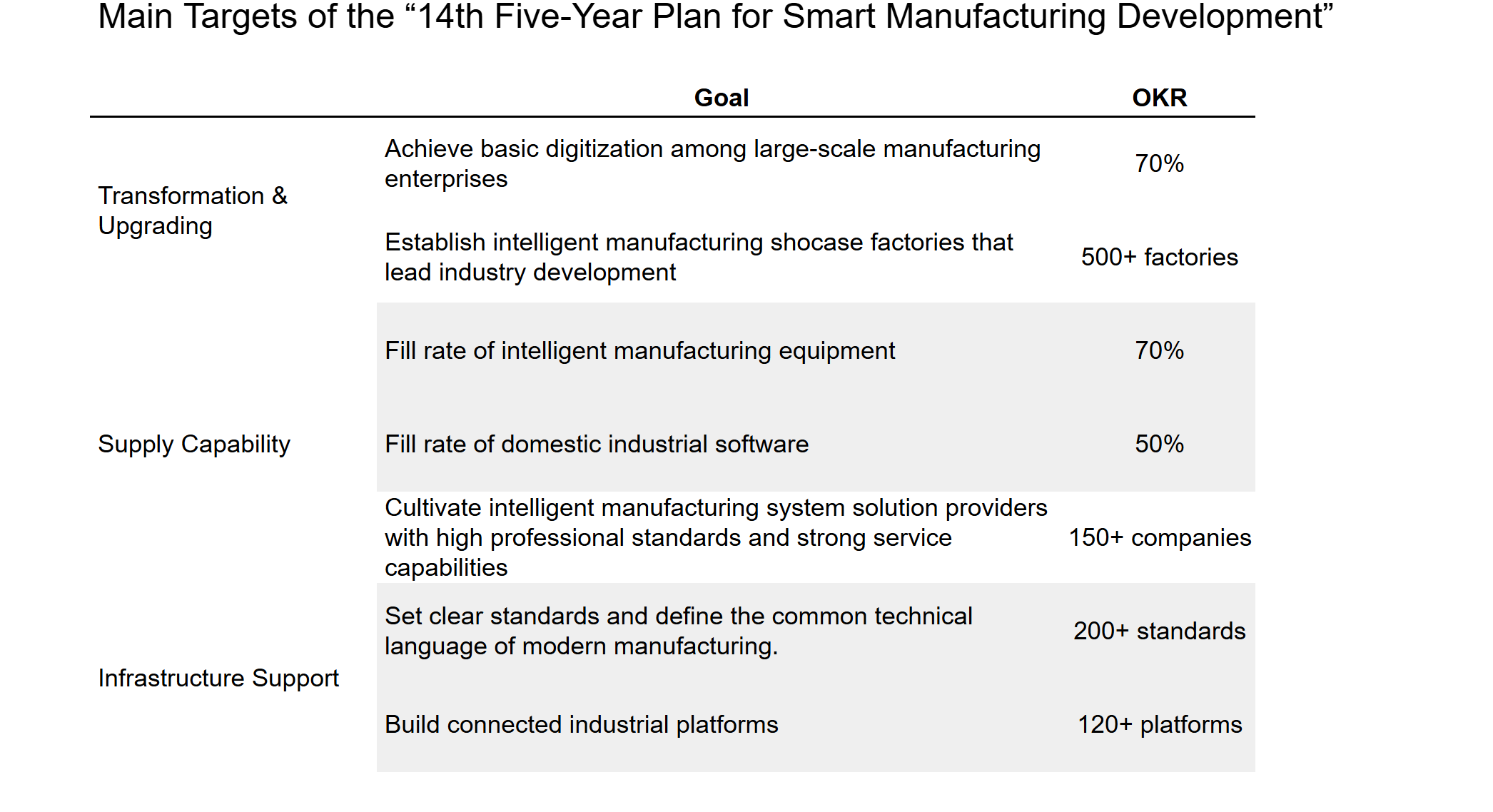

CAD software domestic substitution has become a national priority under China’s 14th Five-Year Plan for Smart Manufacturing Development released in 2020, part of a broader strategy to reduce dependence on foreign industrial software following lessons learned from the 2018 ZTE sanctions crisis, when U.S. export controls nearly crippled the telecommunications giant.

ZWSOFT’s Strategic Acquisition and Kernel Development

ZWSOFT’s progress illustrates a deliberate acquisition-for-capability strategy. In 2010, ZWSOFT acquired VX Corporation, a U.S. geometry kernel developer, using that acquisition as a cold start for building domestic capability. After more than 15 years of development and iteration, this investment yielded the Overdrive kernel, now powering CAD systems used by 1.4 million licensed users across 90 countries, including 149 Fortune 500 corporations. Unlike Open Cascade, which remains primarily in academic and hobbyist use, Overdrive has achieved meaningful industrial adoption at scale3.

The company has invested heavily in R&D infrastructure: six research centers globally (Guangzhou, Wuhan, Shanghai, Beijing, Xi’an, and Florida), with R&D spending consistently at 30% of revenue, far exceeding typical software industry norms of 15-20%. In 2023, ZWSOFT acquired CHAM, a UK-based computational fluid dynamics company, expanding its simulation capabilities beyond pure geometry into multi-physics analysis.

Real industrial deployments demonstrate traction: WELLTEC, a leader in injection molding, uses ZW3D’s integrated solution to streamline design and machining processes. XJ Electric, a global power industry company, leverages ZWSOFT’s IPX engine to revitalize legacy design data and enable one-click import of historical assets4. In June 2024, ZWSOFT released ZW3D 2025 with integrated AI features designed to accelerate design workflows, signaling the company’s move toward kernel-level AI integration.

Huawei’s Multi-Pronged Strategy: Partnership, Enhancement, and Open Source

While ZWSOFT builds the geometry foundation through acquisition and iteration, Huawei is pursuing a sophisticated multi-pronged strategy: partnering to access Russian geometric modeling expertise and massively enhancing the open-source OCCT kernel to build an alternative to Western-controlled CAD infrastructure.

The Nikolay Joint Innovation Center: Accessing Russian Expertise

In February 2024, Huawei partnered with Poisson Software and other Chinese high-tech companies to establish the Nikolay Joint Innovation Center for Geometric Computing. Headquartered in Novosibirsk with branches in Nizhny Novgorod and Moscow, this joint R&D center employs over 400 people, including more than 70 in Russia (with plans to expand to 250). The center focuses on four main areas: creating a new geometric kernel from scratch, optimizing and enhancing the OpenCascade kernel, developing next-generation industrial design software, and building test platforms to validate these technologies. The explicit goal: “surpass SolidWorks.”

OGG 1.0: Open-Sourcing 486 Kernel Enhancements

In November 2023, Huawei made a landmark contribution to the global CAD community by open-sourcing 486 enhanced geometric kernel code improvements to the newly launched OGG (Open Geometry) community. Released as OGG 1.0 at the Cloud Geometry Technology Symposium in Shenzhen, this represents one of the largest single contributions to open-source geometric modeling technology by any company.

OGG is incubated by DISA (Digital Industrial Software Alliance) and operated by Kaiyuan Geometry as a service company, with the stated goal of “providing the world’s industrial software with a second choice.” As DISA Secretary-General Qiu Shuiping explained: “Based on OCCT, the world’s only open-source kernel with engineering value, developing a next-generation industrial software kernel is a strategic choice to ensure continuous and controllable industrial software.”5

The OGG platform is designed as a direct replacement for OCCT, claiming “more features, fewer bugs, and better performance.” As a core contributor to the OGG community, Huawei open-sourced 486 code enhancements representing years of internal development work to Chinese industrial software companies and the global open-source community.

This open-source strategy differs fundamentally from Western approaches. Rather than keeping geometric kernel improvements proprietary, Huawei is building a shared commons of training data, algorithmic improvements, and manufacturing constraints that benefits the entire Chinese CAD ecosystem while positioning OGG as a viable alternative to Western-controlled kernels such as Parasolid and ACIS.

Research and Development Activity

Chinese research institutions are simultaneously advancing AI for mechanical design. A recent paper published in April 2025 demonstrated a generative AI system that reduces required training data from over 16,600 samples to approximately 200 through low-rank adaptation fine-tuning. The system achieved 90% accuracy in generating feasible designs that meet mechanical and manufacturing constraints, with a 30% reduction in overall design time from concept to prototyping preparation6. Researchers at Tsinghua University and other institutions are working on 3D generative models trained on industrial datasets, teaching AI to understand manufacturing constraints from the ground up78.

The Strategic Difference

The key difference between U.S. and Chinese approaches is structural. American innovation is constrained by proprietary kernel monopolies where startups must license expensive infrastructure and remain limited to building application layers. China is creating forcing functions for adoption through a four-pronged approach:

Strategic acquisitions (ZWSOFT acquiring VX Corporation in 2010) that transfer core technology

International partnerships (Nikolay Center) accessing Russian mathematical expertise in geometric modeling

Open-source enhancement (OGG with 486 Huawei contributions) building a shared commons that benefits the entire Chinese CAD ecosystem

Domestic AI research at institutions like Tsinghua achieving 90% design accuracy with 200 training samples versus 16,600

Procurement policies that favor integrated domestic solutions

Whether this multi-pronged approach will produce systems that match the reliability of Parasolid or ACIS, built over 30+ years with thousands of engineer-years of investment, remains to be seen. But the strategy demonstrates sophistication: acquire foundational technology (VX), invest heavily in iteration (15 years for Overdrive), access world-class mathematical talent (Russian partnership), open-source enhancements to build ecosystem adoption (486 OGG contributions), integrate AI at the kernel level, and create forcing functions for domestic adoption, all without dependency on foreign vendors or licensing constraints.

What’s at Stake

Whoever develops the first truly capable foundational AI model for CAD, one that understands geometry, physics, and manufacturing as a unified system, will control a critical layer of industrial infrastructure:

The standard format for design data across design to manufacturing workflows

The interface between AI design and real-world manufacturing

The feedback loops that allow machines to learn from production outcomes and improve iteratively

The problem is that this critical infrastructure layer is monopolized by a handful of players whose business models depend on maintaining closed, proprietary systems. These companies have little incentive to open their geometry kernels to the kind of widespread AI experimentation that drove breakthroughs in language models and image generation.

This monopolization creates a strategic vulnerability for the United States. While American companies control the current CAD market, they’re structurally inhibited from enabling the kind of rapid AI innovation that could define the next generation of manufacturing. Meanwhile, competitors willing to build open infrastructure from scratch, whether through government initiative or coordinated industrial policy, could leapfrog the entire legacy stack.

The real risk is that America’s manufacturing AI capabilities remain stunted by licensing fees and closed architectures while China is building AI-native design systems on open foundations. In a decade, the question may not be “who makes the best CAD software” but “whose AI can design and optimize an entire factory in hours instead of months.”

Control over foundational infrastructure shapes who can innovate, who can compete, and who can build the future without asking permission.

The Path Forward: A Specific Policy Proposal

If the United States wants to maintain its industrial competitiveness, it must recognize geometry kernels as strategic infrastructure, not just commercial software products.

The market has had decades to produce an open alternative and hasn’t, for understandable reasons. Building a commercial-grade geometry kernel requires massive upfront investment with uncertain returns. The network effects around existing kernels, decades of accumulated part libraries, trained engineers, validated workflows, and supplier ecosystems, are nearly impossible to overcome through private capital alone. Venture-backed startups face a cold-start problem: they need industrial customers to validate their kernel, but industrial customers won’t adopt an unvalidated kernel. This is precisely the type of foundational infrastructure problem where coordinated public investment may be justified.

A focused initiative could target a specific beachhead: high-volume tooling for injection molding and stamped parts. Rather than attempting to replace Parasolid across all industries, start where design cycles matter most and validation can happen quickly.

The technical goal would be a kernel optimized for generative design of molds and dies, with deterministic boolean operations, robust NURBS handling, and native support for manufacturing constraints like draft angles, undercuts, and parting lines. Success would be measured not by feature parity with incumbents, but by achieving 10x faster design cycles for the target domain while maintaining reliability demonstrated through a public conformance suite of 10,000+ test cases.

Such an effort would require assembling a world-class team: 12-15 computational geometers and mathematicians to develop core algorithms for curve and surface operations, 6-8 physicists and manufacturing engineers to embed real-world constraints into the kernel’s foundations, 20-25 software architects and engineers to build production-grade infrastructure, and 8-10 validation engineers to test outputs through actual manufacturing runs. This isn’t a project that can be rushed with off-the-shelf tools or outsourced to contractors. It requires sustained collaboration among people who understand how abstract mathematics, physical reality, and manufacturing economics intersect.

The budget would be $150-300 million over 5-7 years, structured as milestone-based grants. On the lower end, a lean 50-person team could deliver a kernel validated for specific operations like injection mold design. The higher end would support a 70-90 person team capable of expanding to adjacent domains and building reference applications that demonstrate real-world adoption.

Governance would run through a nonprofit foundation with an industrial steering group composed of tooling users (automotive OEMs, consumer electronics manufacturers, contract manufacturers) rather than CAD vendors, ensuring the kernel serves manufacturing needs rather than software business models. The IP strategy would use a permissive open-source license for the kernel itself.

Once validated in tooling, the kernel could expand to aerospace secondary structures and fixtures, potentially leveraging government procurement requirements to mandate adoption in defense contracts. Organizations like Convergent Research, which provide 5-7 year funding horizons for focused research organizations, offer an institutional model suited to this type of patient, mission-driven work.

The challenge is substantial. Building a commercial-grade geometry kernel requires both technical skill and manufacturing data for validation. It would need buy-in from industry to test, refine, and eventually adopt the system. It would require sustained funding over years, not quarters. Previous government software initiatives have had mixed results at best, and there’s legitimate skepticism about whether a federally funded project could match the precision and reliability that industrial customers demand.

Yet the alternative is continued dependence on proprietary systems controlled by a shrinking number of vendors, with AI innovation constrained by licensing fees and closed architectures. The question isn’t whether this is difficult, it clearly is, but whether the strategic cost of inaction exceeds the risk of attempting something hard.

Every industrial revolution begins with a new foundational language. In the 18th century, it was the mathematics of thermodynamics that enabled steam power. In the 20th century, it was digital code that enabled computation. In the 21st century, the language may be computational geometry, the mathematical foundation that connects digital designs to physical reality.

Whoever controls that language will shape how the next generation of factories, and nations, are built.

While there isn’t a single definitive academic paper or market analysis that shows CAD software market share, the claim is a well-established observation and industry consensus that can be found in sources such as:https://www.engineering.com/what-is-a-geometric-modeling-kernel/

“CATIA vs. NX 2025: Which CAD Platform Is Best?” CleVR, September 17, 2025. https://www.clevr.com/blog/catia-vs-nx-which-cad-platform-wins. CLEVR

Siemens, How to Manage CAD Software Kernel Data Integrity (white paper). https://resources.sw.siemens.com/en-US/white-paper-how-to-manage-cad-kernel-data/. Siemens Resources

广州中望龙腾软件股份有限公司. 2024 年年度报告摘要 [2024 Annual Report Summary]. 广州: 广州中望龙腾软件股份有限公司, 2025.

广州中望龙腾软件股份有限公司. 2024 年年度报告摘要 [2024 Annual Report Summary]. 广州: 广州中望龙腾软件股份有限公司, 2025.

数字化工业软件联盟 (DISA). “为世界工业软件提供第二选择,Open Geometry Group 1.0 正式发布.” 数字化工业软件联盟, April 22, 2024. https://www.disa.org.cn/Content-244.html.

Li, KY., Huang, CK., Chen, QW. et al. Generative AI and CAD automation for diverse and novel mechanical component designs under data constraints. Discov Appl Sci 7, 315 (2025).

Wang, Chen, Hao-Yang Peng, Ying-Tian Liu, Jiatao Gu, and Shi-Min Hu. “Diffusion Models for 3D Generation: A Survey.” Computational Visual Media 11, no. 1 (2025)

Kim, Jihoon, Yongmin Kwon, and Namwoo Kang. “Deep Generative Design for Mass Production.” arXiv, March 16, 2024.

Incredible piece, I do hope the US can solve this!

https://blog.spec.tech/p/meet-the-2025-brains-fellows?utm_medium=web&triedRedirect=true

See blakes work